Life span, health span and mothballs

How long will I live?...

Hello friends,

I had some lovely responses to last week’s blog Turning 30 and Turning 60. The stand outs were from two readers in their 30s:

“I always find it hilarious when my friends/ family/ peers turn 30 and have a melt down. I’ve always thought aging was such a privilege and always felt glad to be older because older people just always seemed much cooler, less worried and more ‘free’”. Hannah

“How we change through different phases of our lives is something that I find fascinating…maturity of thought and increased emotional intelligence as I get older has definitely been the noticeable shift” Jamie

Nice. Thanks guys. On to today’s musings.

Oh, and if you like what you read please tap the❤️above, or at the end, and subscribe, comment or share: it helps others find my words, and keeps me smiling. Thank you.

A few weeks ago I wrote about 'Enough'. A number of responses asked “well that’s all very well Ruth, but how do I know how much to save when I don’t know how long I’m going to live and how much I will spend?”. And there’s the rub. We don’t know.

The 100 Year Life

The working assumption I used with my financial planning clients was they would live to age 100. “What?” I hear you say “surely your blog should be called ‘2000 Weeks rather than 1000Weeks?” I hear you. But that’s missing the point. A bit.

Death is pretty indiscriminate. None of us know with any certainty when we’ll die. My friend Gordon calls entering your 60s ‘snipers alley’. Charming. Well, he is ex-military.

So, 100 it is unless you give me compelling evidence to the contrary such as a life limiting illness or a strong family history of earlier death. Afterall, it’s not for me to call your mortality but it is mine to have frank and realistic conversations.

Financial Planners makes use of actuarial tables1 to help consider life expectancy and the probability of living long. Here’s some examples of life expectancy for men and women at various ages and the probability of making it to age 100:

The findings bear truth to the old actuarial phrase, “the longer you live, the longer you are expected to live”. If you are married, in a civil partnership or living with your partner, your life expectancy extends further2. Having said that, let’s hope the relationship brings you happiness as well as longevity #justsaying

All models are flawed…

Of course, “All models are flawed, some just may be useful” (attributed to the British statistician George Box3). The advantage of assuming you live to age 100 is that you are unlikely to run out of money. A good start.

The downside of course is that you may die with unspent money in your estate. Depending on your view this may be good or bad. A lovely friend of mine, CJ, has a dread of dying with any money left in her bank account. Her thinking - “what will I have missed out on or not done if I’ve not met this aim?” A resonating truth.

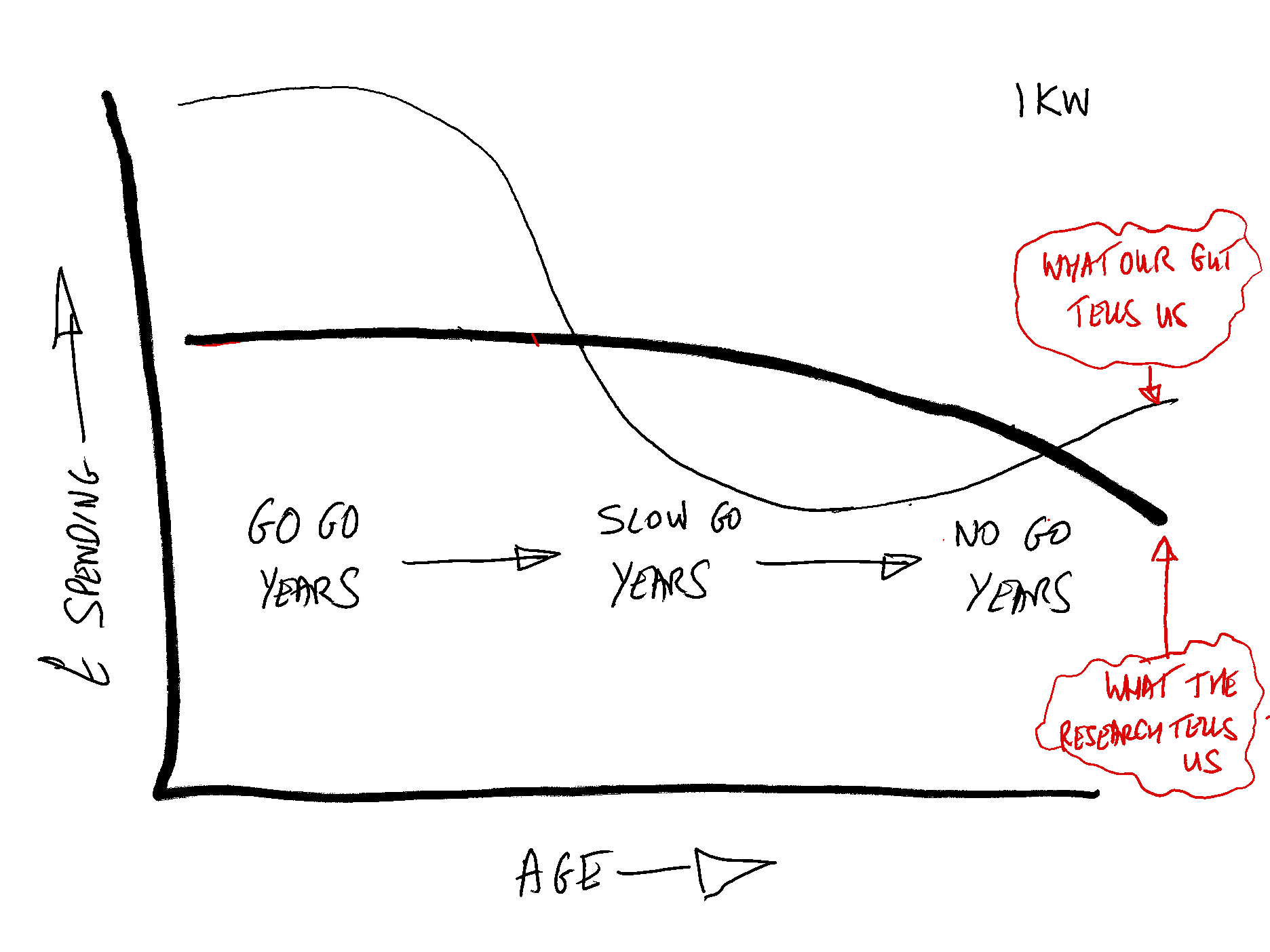

Go Go – Slow Go – No Go

You may be fortunate to live to an old age. But is age enough? Will your health span, the time when you are fit and able to enjoy a full life, match your age span?

I often picture a ‘U Shaped’ spending curve in retirement. In the early years spending is at its peak as you travel, adventure, perhaps move house, buy a campervan or start flying lessons (you never know!). As you move through time spending reduces as desire, energy levels and health slows before moving into a more sedentary stage. A stage which may incur the increased costs of more help at home and maybe some form of care. Interestingly, and in contradiction to this thinking, the research4 shows that for most people expenditure is relatively stable throughout retirement with a slow decline in older age. Nonetheless, instinctively the metaphor of the U Shaped pattern works.

My scribblings below may help visualise these two spending patterns illustrated by the fun phrase the ‘Go Go Years, the Slow Go Years and the No Go years’ describing a typical retirement journey. I’m not going to put ages to these labels, they will be different for us all, but I’m sure you get the gist:

Your reality is likely to be more nuanced.

Don’t mothball your life

None of us know how long our current state of health will be maintained.

The potential of later life care and affordability may be a concern, but I would argue it should not be at the expense of living a full life when you are able. Most don’t need care, certainly not in the inheritance gobbling, bankruptcy inducing way the media would have us believe. As I said, this is nuanced. The assistance of a good financial planner will definitely help you figure this out. But don’t mothball life today, just in case you live long.

Which brings me to the key point. What are you waiting for? You are never going to be any younger than you are today. You may well never be any fitter than you are today. If there are things you want to do, get on and do them now. Be that spike in my U Curve. Go on, go for it.

Let me know what ‘spikes’ you have made or intend to make, I’d love to hear from you.

Until next time my friend,

Ruth x

Hat-tip to my friend Brian Portnoy founder of Shaping Wealth and author of The Geometry of Wealth for introducing me to this phrase

I'm so glad I read this after just today treating myself to a new designer handbag.